DEVELOPERS

RESOURCES

RWA perps carry oracle requirements that crypto perps do not. Commodities trade on fixed schedules with weekend closures. FX pairs have daily one-hour maintenance windows. Equity markets open and close with gap risk at the bell. Commodity futures contracts expire and roll on different timelines depending on the underlying.

Standard oracle feeds treat all assets the same way. A single aggregation method, a single update cadence, a single approach to market hours. That works for BTC/USD. It breaks for commodities with volatile calendar spreads, where medianizing across providers tracking different futures contracts produces unreliable prices around market reopen. It breaks for equity perps, where the overnight gap can move a stock 10% on earnings.

Ostium took an opinionated approach to this problem. Rather than adapting generic feeds, the team built custom pricing logic for each asset class and partnered with Stork to run it at production scale.

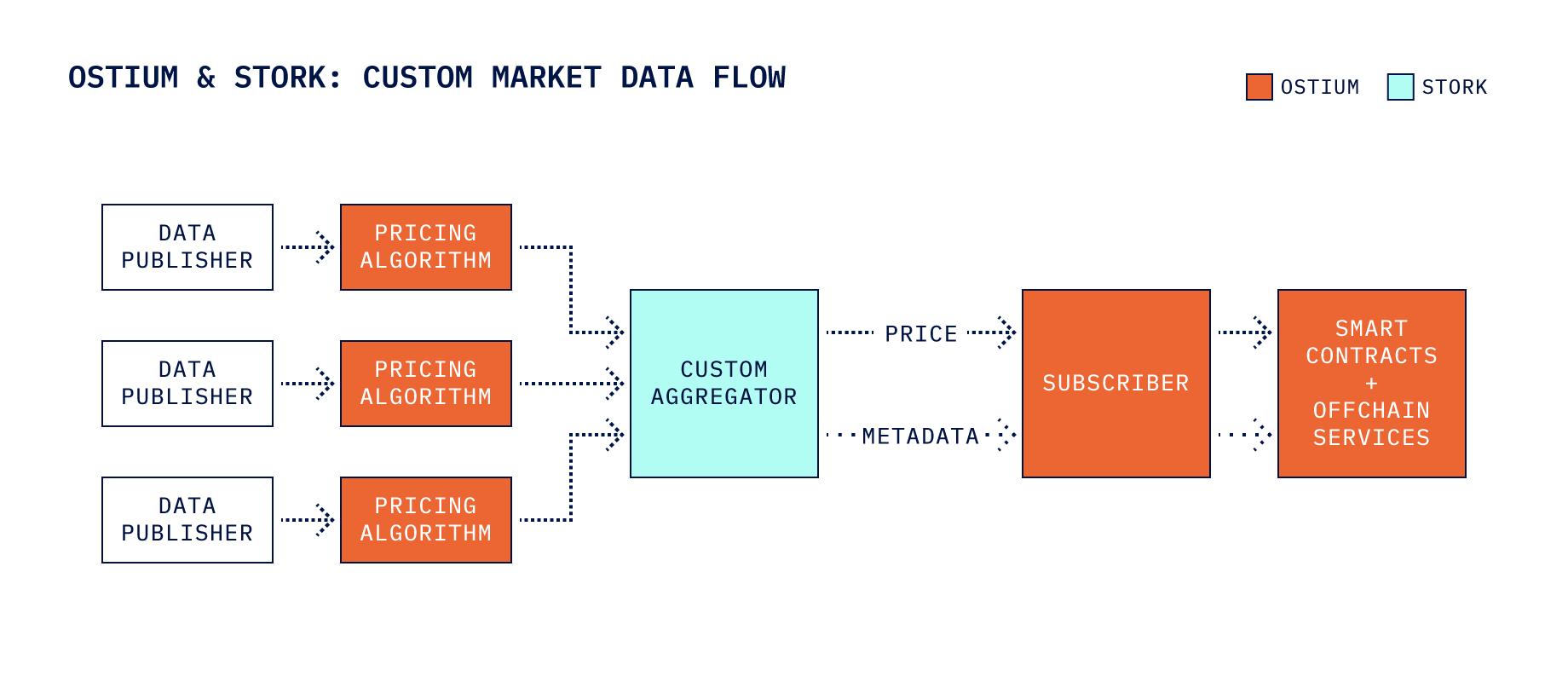

Stork worked with Ostium to build a bespoke RWA oracle pipeline. The architecture has three layers.

Data sourcing: Multiple data providers run Ostium’s algorithm for supported assets.

Custom aggregation: Stork operates a modified aggregator, custom-built to parse Ostium's unique pricing algorithm output. This aggregator processes metadata such as market hours and orderbook data, including them in price reports. The metadata allows Ostium to support users with exceptional portfolio risk management capabilities.

Onchain delivery: Data flows from the Stork-operated custom aggregator into an Ostium subscriber that pushes price updates onchain as needed. This keeps costs viable for long-tail assets that would be uneconomical under a push-based model. Learn more in the Ostium docs.

Stork worked closely with Ostium’s team to develop custom aggregation logic to accommodate the unique characteristics of each asset class.

Commodities require careful handling of futures contract rolls.

FX pairs trade nearly 24 hours on weekdays but close on weekends with a one-hour daily maintenance window.

Equity perps introduce overnight gap risk, earnings-driven volatility, and trading-hour constraints that commodity and FX markets do not share.

Ostium now lists 55 assets, including 22 stocks (such as NVDA, TSLA, AAPL, MSFT, GOOGL, META, AMZN, and COIN) and seven indices (such as S&P 500, Nikkei 225, Hang Seng, and FTSE 100). Each feed requires market-hours enforcement, holiday calendars, and gap-risk-aware pricing at open. Stork's per-asset oracle architecture made this expansion possible without rebuilding the oracle layer. (Read more here on the oracle challenges specific to equity perps.)

In August 2025, Ostium launched 0DTE (zero days to expiry) perpetuals for equities. These instruments offer up to 100x intraday leverage on individual stocks, with positions automatically reduced or closed before market close to eliminate overnight gap risk.

Stork's existing metadata infrastructure extended naturally to support this new instrument type, providing the market-close timing signal that triggers automatic position wind-down.

Ostium has grown to over $45B in cumulative trading volume, including $5B in metals alone. Over 95% of open interest sits in traditional markets, meaning Stork's custom RWA feeds carry nearly all of the protocol's risk exposure.

During the 2025 gold rally, Ostium captured more than 50% of total on-chain gold perpetuals open interest. Stork and Ostium worked together to position the exchange to capture this activity, delivering proof of perpetual futures’ potential for macro assets and a live stress test of Stork's commodity oracle feeds under sustained directional flow and elevated volatility.

Ostium frames its competition as the global contract-for-difference (CFD) broker market, not other perp DEX platforms. CFD brokers collectively process an estimated $10T in monthly volume, but they operate on opaque, discretionary infrastructure. Brokers control pricing, liquidation thresholds, and withdrawals. Traders have no way to verify execution quality or confirm that spreads match advertised levels.

Perp DEXs solve this structurally. Every trade, spread, and liquidity parameter is visible onchain. Collateral stays in segregated smart contracts under the trader's control. Liquidation logic is deterministic and auditable. The oracle layer, powered by Stork, provides the same verifiability: prices are cryptographically signed by known publishers, and delivered through onchain infrastructure that anyone can inspect. The CFD opportunity represents a potential doubling in size relative to 2025’s $93T volume in the perpetual futures market as estimated in CoinGecko’s 2025 annual report.

Ostium's $24M Series A, co-led by General Catalyst and Jump Crypto in December 2025, brought total funding to $27.8M and validated the thesis that onchain infrastructure can compete with legacy brokers at scale. Investors include Coinbase Ventures, Wintermute, Jump Crypto, Balaji Srinivasan, LocalGlobe, Susquehanna International Group (SIG), Crucible Capital, GSR, Nick Van Eck, Shiliang Tang, and angels from Bridgewater, Two Sigma, and Brevan Howard.

Equity and RWA perps remain early. The category barely existed two years ago. Ostium's trajectory, from testnet to $45B in volume and broad coverage across asset classes, shows that traders want on-chain access to traditional markets when the infrastructure supports it. As Ostium expands into new asset classes and geographies, Stork's custom oracle architecture is the pricing layer that brings these markets onchain.